")

The National Social Assistance Programme (NSAP), launched by the Government of India in 1995, represents a significant commitment to fulfilling the Directive Principles of State Policy enshrined in the Constitution, particularly Article 41, which mandates the State to provide public assistance to its citizens in cases of undeserved want, including old age, sickness, and disablement.1

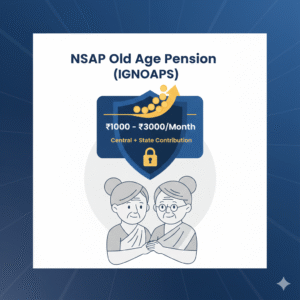

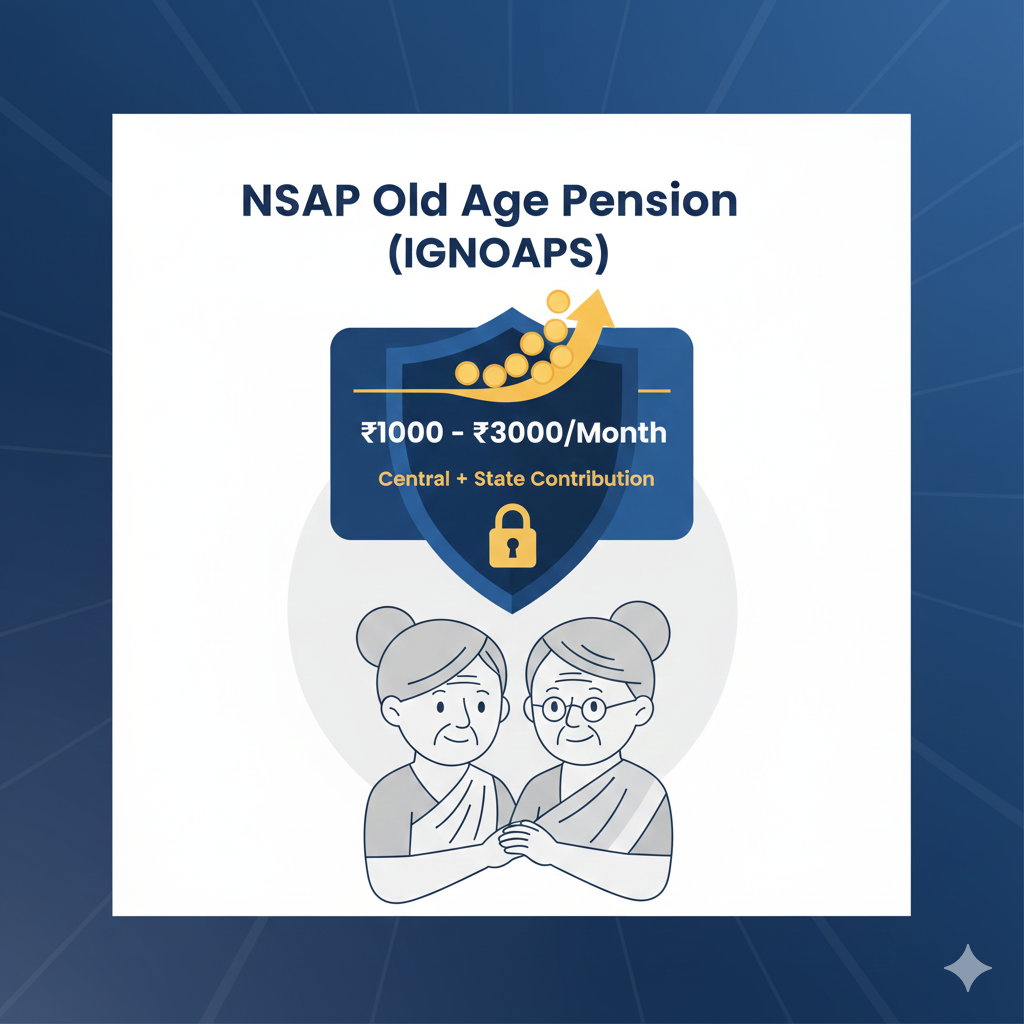

NSAP is a welfare programme aimed at providing a minimum national standard of social assistance to vulnerable households across the country.2 While the programme encompasses several sub-schemes for widows, disabled persons, and family benefits, its most widely recognized and crucial component is the Old Age Protection provided under the Indira Gandhi National Old Age Pension Scheme (IGNOAPS). This scheme ensures that the poorest senior citizens receive a regular, non-contributory monthly income to secure a life of dignity.3

🎯 The Core Objective: Protecting the Destitute Elderly

The original and central objective of the NSAP, particularly IGNOAPS, was to provide social assistance to destitute individuals. This category was defined as:

- Any person who has little or no regular means of subsistence from their own source of income.4

- Someone who has little or no financial support from family members or other sources.5

While the criteria were later expanded to cover all persons Below the Poverty Line (BPL), the core philosophy remains the same: ensuring that the most vulnerable and financially insecure citizens are not left unprotected in their final years.6

Eligibility Criteria for Old Age Protection (IGNOAPS)

The scheme is meticulously targeted to reach the neediest senior citizens, primarily relying on the Below Poverty Line (BPL) classification.7

- Citizenship: The applicant must be an Indian Citizen.8

- Poverty Status: The applicant must belong to a household Below the Poverty Line (BPL), as identified by the Central Government’s criteria (although many states have expanded this to include non-BPL families using their own funds).9

- Age: The applicant must be 60 years of age or above.10

The scheme is entirely non-contributory, meaning the beneficiary does not have to pay any premium or make any contribution to receive the pension.11

💰 The Financial Structure: A Collaborative Pension

The unique aspect of NSAP is its nature as a Centrally Sponsored Scheme (CSS), where the final benefit is a joint responsibility of the Central Government and the respective State/Union Territory Governments.12 This ensures that while a basic minimum is guaranteed by the Centre, states are encouraged to supplement the amount based on their economic capacity, leading to significant variations in the total pension received.13

Central Government Contribution (IGNOAPS)

The Central Government’s financial assistance is divided based on the age of the beneficiary:14

| Age Group | Central Contribution (Per Beneficiary/Month) |

| 60 to 79 years | Rs. 200/- |

| 80 years and above | Rs. 500/- |

The search results indicate that the initial information provided in the prompt stating a Central Contribution range of $Rs. 300$ to $Rs. 500$ may be slightly simplified, as the current official Central contribution for the 60-79 age group under IGNOAPS is $Rs. 200/-$, and $Rs. 500/-$ for those 80 and above. The $Rs. 300/-$ figure might represent an older revision or include a minimum state contribution in some contexts.

State Contribution and Final Pension Amount

The prompt mentions that the Monthly pension ranges from $Rs. 1,000/-$ to $Rs. 3,000/-$ (or even higher) depending upon the state’s contribution.

This high variability underscores the collaborative structure:

- States and UTs are strongly urged to provide an additional top-up amount at least equivalent to the Central contribution.15

- Many progressive states provide a substantially higher top-up, leading to a much larger final pension amount for the beneficiary.16 For instance, some states provide total monthly pensions ranging from $Rs. 1,000/-$ to over $Rs. 4,000/-$ by significantly boosting the Central share.

This state top-up mechanism is crucial because the base Central contribution alone is often considered insufficient to meet the basic needs of a senior citizen, especially in high-cost urban environments.

🫂 The Broader NSAP Framework: More Than Just Old Age

While IGNOAPS is the most prominent component, the NSAP is a comprehensive package encompassing five schemes aimed at different aspects of social vulnerability :

- Indira Gandhi National Old Age Pension Scheme (IGNOAPS): The focus of this article, providing old age income security.17

- Indira Gandhi National Widow Pension Scheme (IGNWPS): Provides monthly financial assistance to BPL widows aged 40 years and above.18

- Indira Gandhi National Disability Pension Scheme (IGNDPS): Provides monthly financial assistance to BPL persons aged 18 years and above with severe or multiple disabilities.19

- National Family Benefit Scheme (NFBS): Provides a one-time lump sum assistance of 20$Rs. 20,000/-$ to BPL households upon the death of the primary breadwinner (aged 18-59 years).

- Annapurna Scheme: Aims to provide food security to senior citizens who are eligible for IGNOAPS but are not covered under the scheme.21 It provides 10 kg of free food grains per month.22

These components collectively form a vital social security floor across the country, ensuring basic assistance during life events such as old age, loss of the breadwinner, and disability.23

🏛️ Implementation and Administrative Mechanism

The NSAP is administered by the Ministry of Rural Development, Government of India.24

- Implementation: The schemes are implemented in both rural and urban areas by the respective Social Welfare Departments of the States/UTs.25

- Identification: Beneficiaries are primarily identified using the official BPL list prepared by the State/UT governments.26

- Disbursement: Funds are typically transferred directly to the beneficiary’s bank or post office account through Direct Benefit Transfer (DBT), enhancing transparency and reducing leakage.27 The process is designed to be administered at the local level through Panchayats and Municipalities, making it responsive to local needs.28

Significance and Challenges

The NSAP represents India’s commitment to building a welfare state as envisioned by the Constitution.29 It achieves the following:

- National Minimum Standard: It ensures that every eligible citizen, regardless of their state of residence, receives a minimum level of social protection.30

- Poverty Alleviation: The guaranteed monthly income directly tackles old-age poverty and provides financial autonomy to senior citizens.

- Constitutional Compliance: It is a core instrument for fulfilling the mandate of the Directive Principles of State Policy.31

However, the scheme faces challenges, primarily concerning the low level of the Central contribution, which has not been substantially revised in years. The significant reliance on state top-ups leads to wide disparities in the actual pension received across states, making the goal of a uniform “minimum national standard” difficult to achieve in practice.32 Nonetheless, the NSAP remains the single most important non-contributory mechanism providing a lifeline to India’s vulnerable elderly and households